“It’s a hard day,” read the email subject line to Shelly Little from her bosses at Carvana, an online used car retailer.

The note signalled Little was one of almost 2,500 staff laid off from the US-based company this week, in a mood described by another employee as “mass hysteria”. Since the start of the year, stock in the company famed for its towering multistorey car “vending machines” has fallen 87 per cent.

“As the ramifications of that kicks in all I can think is — wow,” Little wrote on LinkedIn, informing her friends and coworkers that she was one of the 12 per cent at Carvana being shown the door.

Her experience reflects the sudden sobriety that has descended over the US technology sector, prompted by a deep and broad stock sell-off as investors fret over rising interest rates and slowing economic growth.

Privately held companies are being forced to readjust expectations on valuations, access to funding and appetite for risk-taking among venture capitalists that may no longer throw caution to the wind.

“I think it’s certainly humbling for a lot of people in technology who thought things would never go another way, or didn’t plan for a rainy day, or were being a little bombastic,” said Semil Shah, a founder and general partner at San Francisco-based venture capital firm Haystack.

“If you were really counting your chickens before they hatched, or you were thinking about all the riches that would come your way, it’s going to take a while.”

In the public markets, Carvana has been one of the worst hit, but it is by no means alone. DoorDash, the US market leader for restaurant food delivery, is down 60 per cent year to date. Affirm, one of the biggest in the previously highly-fancied buy-now-pay-later sector, has crashed 85 per cent. Shopify, the ecommerce operator regularly billed as the most serious threat to Amazon’s ecommerce dominance, is down 77 per cent.

Even Big Tech companies, some of the surest growth stocks for the past decade, have suffered large drops. Apple, Amazon, Alphabet and Meta have collectively seen $2.1tn wiped off their market capitalisations. In Apple’s case, its $600bn dip was enough to see it dethroned this week by Saudi Aramco as the world’s most valuable publicly traded company.

That an energy giant should take over its mantle is illustrative of the shift in investor confidence from companies with strong top-line growth but shakier bottom lines to those that are surer bets, said Brent Thill, an analyst with Jefferies.

“It’s a full-scale, complete puke of tech, a full-fledged eject button,” he said. “Less than a year has gone by and all high-growth software companies are now evil with no profits. I think it’s a wholesale shift out of tech into defensive sectors, energy and utilities.”

Tech companies are reacting by tackling the basics — cutting costs, reducing cash burn and focusing on the fundamentals.

“I’ve been talking about free cash flow more than I think I have since I took my first accounting class, it’s kind of wild,” said one person at a major public tech company.

Similarly, at Uber, with its stock down 49 per cent this year, chief executive Dara Khosrowshahi told staff in a memo last weekend: “The goalposts have changed. Now it’s about free cash flow.”

“In times of uncertainty, investors look for safety,” he added in the note, first reported by CNBC and verified by the Financial Times. “They recognise that we are the scaled leader in our categories, but they don’t know how much that’s worth. Channelling Jerry Maguire, we need to show them the money.”

After dramatically renaming and reorienting his company last year, Meta chief executive Mark Zuckerberg’s eagerness around the metaverse has made way for a more clipped enthusiasm for big investment. The social media company last month pledged to reduce its spending forecasts by several billion dollars across this year.

To achieve it, Meta has pulled the handbrake on aggressive headcount growth. According to an internal memo from Meta’s chief financial officer David Wehner, obtained by the FT, it recruited more employees in the first quarter of this year than in the whole of 2021 — but this has come to an end.

“We need to take another look at our priorities and make some tough decisions about what projects we go after in both the short and medium term to achieve the lower expense guidance we committed to during earnings,” he wrote, adding: “This will affect almost every team in the company.”

Another Meta executive’s note said scheduled job interviews for what would have been prospective junior and mid-level engineering employees will be “sensitively cancelled”.

Twitter, potentially on the brink of takeover by Elon Musk, said on Thursday it had not met its own “intermediate milestones” for growth, so it was “pulling back on non-labour costs to ensure we are being responsible and efficient”.

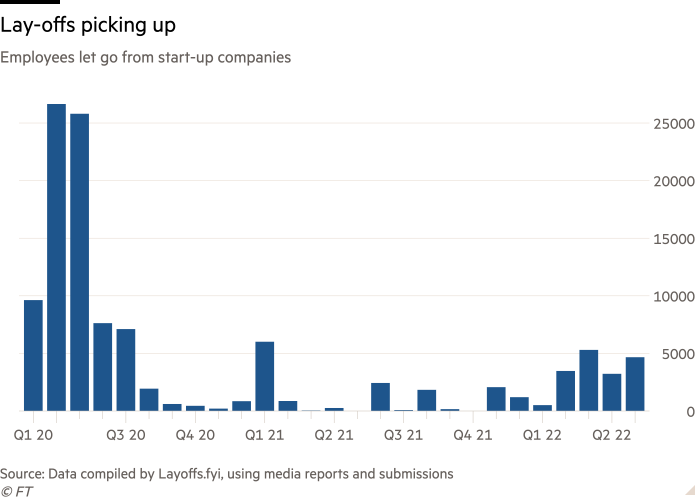

Companies across the tech sector are taking a close look at headcount as an immediate way to cut costs. Layoffs.fyi, a site that tracks lay-offs among public and private tech start-ups, has logged a surge beginning in February, though levels are still way below the early stages of the coronavirus pandemic. Delivery “ghost” kitchen start-up Reef, celebrity shout-out platform Cameo and dieting and wellness app Noom are among the private companies shedding staff.

How the tech sell-off begins to impact the private sector, and the financing ecosystem that underpins it, is only just beginning to be felt.

According a report published by analytics group PitchBook this week, companies closest to moving to the public markets and seeking to raise larger rounds have been the first to experience a headwind, experiencing a “much different sentiment from investors” compared to valuation highs in 2021.

According to CB Insights, global venture capital funding in the first quarter of 2022 was down 19 per cent on the previous quarter, the largest percentage drop since the third quarter of 2012. The number of public exits — whether by initial public offering or Spac merger — was down 45 per cent.

Haystack’s Shah said money for start-ups has already become harder to come by for companies without a firmly established business model.

“People are still writing cheques,” he said. “But if you’re raising 500k, or 5mn or 50mn, you have to fight for it — much more than you would have had to fight for it a year ago.”