Eyeing the prices at a Budapest market hall, retired school nurse Maria Veres said she was grateful for a big January pension bonus from Viktor Orban’s government. It encouraged her to vote to re-elect the premier this month, but the windfall is almost gone already.

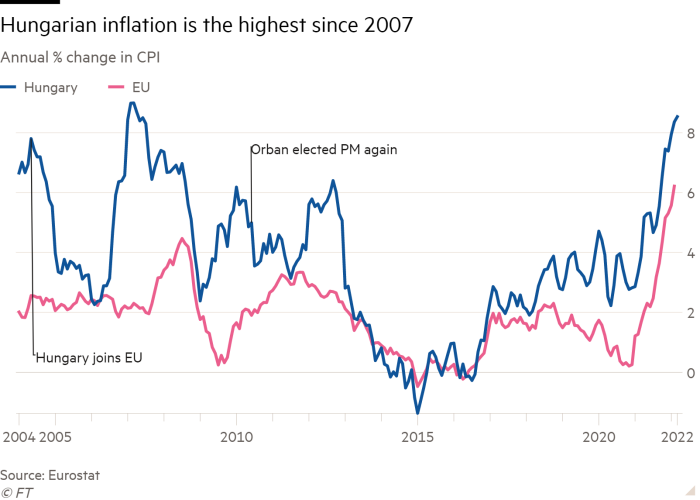

Hungary’s highest inflation in 15 years is cutting into her freshly padded savings but has not yet hit her confidence in Orban, who she expects can protect citizens from rising prices and other economic problems.

“These price tags are horrific,” she said, looking at a dozen eggs costing about 600 forints, or just over €1.50, up one-third from a year ago. “This sort of inflation, I thought it was a thing of the past. I hope Orban defends us from this somehow.”

While he is buoyed by a fourth consecutive election win that extends his tenure as the EU’s longest-serving leader, Orban — who has said he is determined “to preserve financial stability” — faces some of the biggest economic challenges of his time in office.

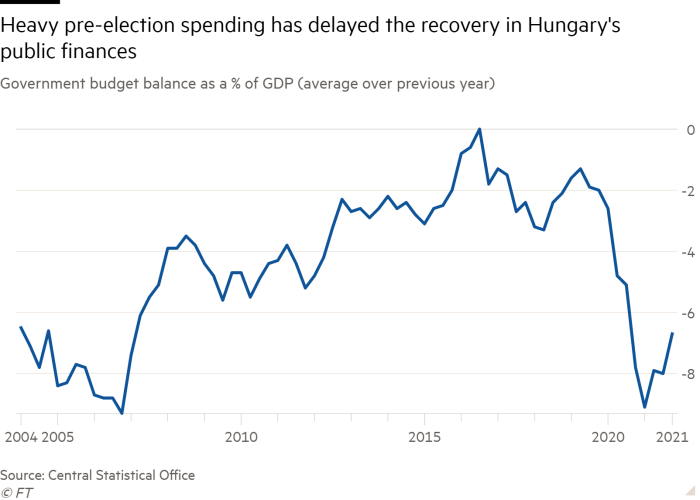

Soaring energy costs are straining Hungary’s ability to maintain state-imposed price caps, while global disruption from Russia’s invasion of Ukraine is denting prospects for growth. Heavy pre-election spending, and a row with Brussels that is delaying more than €7bn in EU aid, is further constraining room for economic manoeuvre.

The EU funds are meant to finance projects to boost Hungary’s recovery from the pandemic. Orban wants to borrow the funds in the meantime but analysts said that would increase Budapest’s debt levels and financing costs.

“If we can access [recovery funds], we will have to take smaller steps toward the financial market; if not, then we will be forced to take larger ones,” Orban told journalists this month, calling the strategy “prefinancing” until the EU money arrives.

Part of the squeeze on Hungary’s finances stems from Orban’s generosity in the run-up to the April 3 election. The government gave away about €5bn in the first quarter in family tax rebates and pension bonuses. It also now faces lower growth and tax receipts because of the economic disruption caused by the Ukraine war.

KBC’s Hungarian economist David Nemeth said the EU funds “would go a long way to help solve the budget problems” for Orban, who could then spend more on maintaining price caps and other measures to fight inflation.

Despite his need for EU cash, Orban has said he will not make concessions to improve relations with the EU. “No matter the pressure on us, we will never back down,” Orban said.

Fitch Ratings said this month that Orban’s clear election victory, and Brussels’ decision to start a process to penalise alleged rule of law abuses in the country, “could signal a hardening of both sides’ stances” and threaten growth forecasts.

It also warned that a deterioration in governance standards in Hungary could undermine investor confidence and affect the country’s credit rating. Budapest’s rating is now two notches into investment grade with a stable outlook from all three major rating agencies.

Lower ratings would raise borrowing costs. A negative spiral of higher debt, rising debt payments and lower credit ratings is a possibility, said Peter Oszko, Hungary’s last finance minister before the Orban era, which began in 2010.

“Market debt is very expensive, hurts the budget balance, the interest on it is rising, but [Orban] can tap that for a while, hoping for an agreement with the EU,” said Oszko. “Time is tight but he will try to take his time, try a few vetoes, form a few alliances.”

Oszko said the government should worry most about inflation. “Orban is not afraid to levy extra taxes on lucrative business sectors or issue bonds, as long as he can avoid leaning on the voters directly,” he said. “But a sustained double-digit inflation rate hurts everyone.”

Gergely Suppan, an economist at Takarekbank, said he expected Orban would halt investment or allow the budget deficit to exceed 5 per cent, compared with the EU’s usual 3 per cent limit, before he touches price caps, which keep gas bills below €100 a month for an average household, far below western Europe’s.

“If market prices were introduced, most people would fail to pay their bills,” said Suppan. “Utility prices have not changed since 2014, during which time net salaries more than doubled. We could handle 10, 20 per cent, but a fivefold increase would be nonsensical.”

Orban has not ruled out more taxes on sectors like finance, energy, telecommunications and retail. “Whether special taxes on multinationals or others become necessary is up to the EU,” he said. “If Europe is unable to halt the energy price increase, we will be forced to take steps in Hungary.”

Peter Virovacz, an economist with ING, said a fiscal adjustment of about 1 per cent of gross domestic product could be achievable via spending cuts but greater recalibration would mean tax increases.

“We wouldn’t expect measures affecting the tax burden on labour but rather some sectoral taxes [in] banking, telecommunication and/or retail,” Virovacz said. “The caveat with these could be that companies will pass on the costs to households — which would strengthen inflation further.”