Global bond markets posted a powerful rebound in the first fortnight of 2023, fanning investors’ hopes that last year’s fixed-income retreat is over.

Bonds are on track for their best January performance in more than three decades, spurred by a growing conviction that inflation has peaked on both sides of the Atlantic.

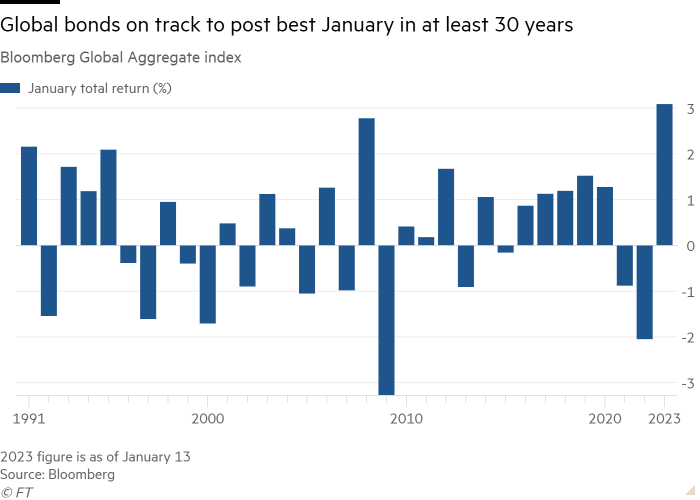

The Bloomberg Global Aggregate index, a broad gauge of global fixed income, has delivered a 3.1 per cent return so far this month. If that continues for the rest of January it will be the biggest rise logged in the first month of the year in records going back to 1991. The index fell by more than 16 per cent in 2022.

“It’s like night and day,” said Richard McGuire, a fixed-income strategist at Rabobank. “Last year was historically bad but there’s every sign that this one is going to be much better for bond investors. Growth is slowing, inflation is decelerating and we are confident that the peak in policy rates has already been priced.”

Investors are betting that the Federal Reserve and European Central Bank will move more slowly this year in their efforts to tame rising prices, after both central banks helped to capsize debt markets last year by raising interest rates at an unprecedented pace.

At the same time, the spectre of a looming recession could damp appetite for riskier assets such as stocks and instead draw big flows of money to the safety of highly rated government debt.

The gains — driven by a big rally in long-term government debt — are an early vindication for fund managers who in December favoured bonds in their portfolios relative to other asset classes for the first time since 2009, according to Bank of America’s closely watched monthly investor survey.

The 10-year US Treasury yield has fallen to 3.46 per cent, from 3.83 per cent at the end of 2022, reflecting a surge in price. Germany’s 10-year yield, a benchmark for the euro area, has dropped from 2.56 per cent to 2.10 per cent in the same period.

Data in the first week of January showing that eurozone inflation fell faster than expected last month as energy prices dropped, helping trigger the global bond rally. Meanwhile, confirmation this week that US inflation dropped to its slowest pace in more than a year at 6.5 per cent in December helped to cement the gains.

Investors started the year already betting that the Fed would begin cutting interest rates later in 2023 as the US economy slows, despite repeated statements by central bank officials that borrowing costs may have to remain high for some time to curb inflation.

But even if rate cuts do not materialise, some investors argue that waning inflation diminishes the uncertainty around further large increases, which should benefit longer-term bonds as well as riskier types of debt.

“The Fed is eventually going to get to a plateau,” said Steven Abrahams, head of strategy at Amherst Pierpont. “At a certain point this year, major shifts in Fed funds will be off the table, which should materially reduce interest rate volatility. And as rate volatility comes down, risk assets, mortgage-backed securities and corporate credit should do well.”

There is also a widespread hope that bonds will regain their traditional role as a safe place to shelter from the coming economic downturn and should gain if equity markets suffer. That would mark a break with 2022’s synchronised sell-off when bonds dropped even though the MSCI All-World stock index shed almost 20 per cent.

“It is very rare to have a big down year for both stocks and bonds, and last year was the first time since 1974 where you had both down,” said David Kelly, chief global strategist at JPMorgan Asset Management. “You typically bounce the following year, and I think that’s what is happening now. It is not the best of times, but it is not the worst of times either.”

Others detect a whiff of complacency in the bond market resurgence. The faith in markets that rates are nearing their peak, and cuts are on the way, is at odds with central banks’ newfound insistence that they will do whatever it takes to quell inflation, according to Mark Dowding, chief investment officer at BlueBay Asset Management.

“We are doubtful that the relatively strong market conditions at the start of 2023 can be sustained for too long,” Dowding said, adding that he is “concerned by a narrative in markets that we don’t need to listen to central banks, as they don’t matter very much”.

“This may seem complacent and we learned in 2022 just how quickly underlying conditions can change.”