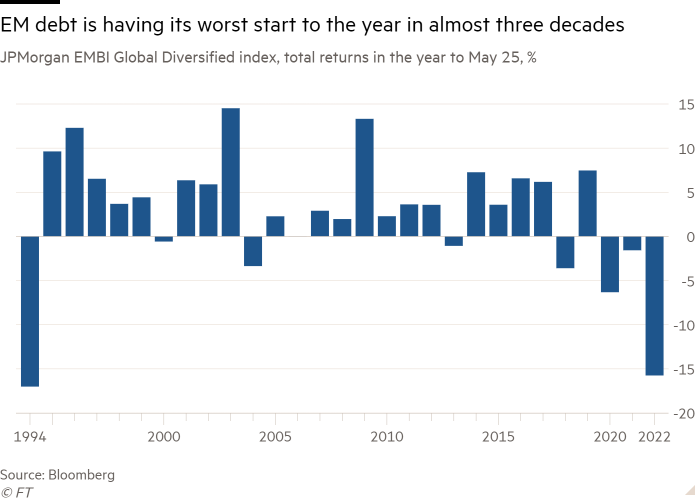

Emerging market bonds are suffering their worst losses in almost three decades, hit by rising global interest rates, slowing growth and the war in Ukraine.

The benchmark index of dollar-denominated EM sovereign bonds, the JPMorgan EMBI Global Diversified, has delivered total returns of around minus 15 per cent so far in 2022, its worst start to the year since 1994. The decline has only been slightly eased by the broad rally across global markets in recent days, which ended a seven-week losing streak for Wall Street stocks.

Nearly $36bn has flowed out of emerging market mutual and exchange traded bond funds since the start of the year, according to data from EPFR; equity market flows have also gone into reverse since the start of this month.

“It’s certainly the worst start I can remember across the asset class and I’ve been doing EMs for more than 25 years,” said Brett Diment, head of global emerging market debt at Abrdn.

Developing economies were hit hard by the coronavirus pandemic, straining their public finances. Rising inflation, slowing global growth and the geopolitical and financial disruption caused by Russia’s war in Ukraine have added to the economic pressures they face. The investment outflows threaten to worsen their woes by tightening liquidity.

David Hauner, head of EM strategy and economics at Bank of America Global Research, said he expected the situation to get worse.

“The big story is that we have so much inflation in the world and monetary policymakers continue to be surprised by how high it is,” he said. “That means more monetary tightening and central banks will continue until something breaks, the economy or the market.”

Yerlan Syzdykov, global head of emerging markets at Amundi, said higher yields in developed markets like the US — driven by central banks’ rate rises — make EM bonds less attractive. “At best you will make zero, at worst you will lose money [this year],” he said.

Hauner said that rate rises in major developed market economies were not necessarily bad for EM assets if they were accompanied by economic growth. “But that is not the case now — we have a major stagflation problem and central banks are raising rates to kill rampant inflation in some places, such as the US. This is a very unhealthy backdrop for emerging markets.”

China, the world’s biggest emerging market, has faced some of the heaviest selling.

Concerns about geopolitical risk, including the possibility that China will invade Taiwan in the wake of Russia’s invasion of Ukraine, had been exacerbated by the economic slowdown as the government imposed draconian lockdowns in pursuit of its zero-Covid policy, said Jonathan Fortun, economist at the Institute of International Finance, which monitors cross-border portfolio flows to emerging markets.

Chinese assets have received large so-called passive inflows over the past two years, he noted, following the country’s inclusion in global indices which meant that fund managers attempting to mirror their benchmarks automatically bought Chinese stocks and bonds.

This year, however, such flows had gone into reverse, with more than $13bn leaving Chinese bonds in March and April and more than $5bn leaving Chinese equities, according to IIF data.

“We are pencilling in negative outflows from China for the remainder of this year,” Fortun said. “This is a very big deal.”

Fund managers have not allocated some of the money withdrawn from China to other EM assets, he said, resulting in a widespread retreat: “Everyone is turning from the whole EM complex as an asset class and going to safer assets.”

The shock to commodity prices caused by the war in Ukraine has added to the strain on many developing countries that rely on imports to meet their needs for food and energy.

But this has also delivered some winners among commodity exporters. Diment at Abrdn noted that, while local currency bonds in the JPMorgan GBI-EM index have delivered total returns of minus 10 per cent so far this year in dollar terms, there is wide divergence between countries.

Bonds issued by Hungary, which is close to the war and relies on Russian energy imports, have lost 18 per cent in the year to date. Those of Brazil, a big exporter of industrial and food commodities, are up 16 per cent in dollar terms.

Diment said valuations of EM debt “arguably look pretty attractive now” and that Abrdn has seen net inflows so far this year into its EM debt funds.

However, Hauner at Bank of America argued that the bottom will only be reached when central banks shift their attention from fighting inflation to promoting growth. “That may happen sometime by the autumn but it doesn’t feel like we are there yet,” he said.

Syzdykov said it depended on whether the surge in inflation ebbs, returning the global economy to an equilibrium between low inflation and low interest rates. The alternative is that the US goes into recession next year, adding to the drag on global growth and pushing EM yields higher still, he warned.