Money has already evolved from coins, to notes, entries in balance sheets and bits on computers. The institutions that provide, operate, guarantee and regulate money have evolved with it. So how should it evolve in the digital era? The invention of cryptocurrencies has forced everybody involved and above all the central banks — the agents of the state in managing the public good of money — to confront this question. If crypto is not the answer, what is?

The Bank for International Settlements — the club of central banks — has been prominent in the effort to address this question. The latest result is part of its Annual Report, which analyses the emerging ecosystem of cryptocurrencies, stablecoins and exchanges.

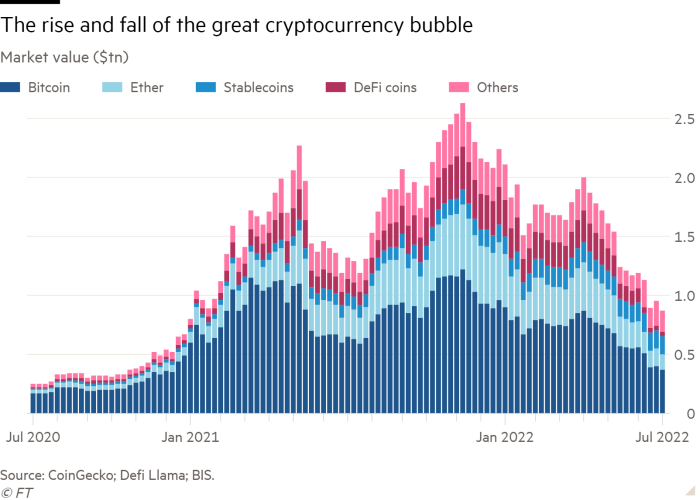

This brave new system is — it concludes — inherently flawed. The crypto crash (and preceding bubble) shows that cryptocurrencies are objects of speculation rather than stores of value. That also makes them unusable as units of account. As the BIS notes: “The prevalence of stablecoins, which attempt to peg their value to the US dollar or other conventional currencies, indicates the pervasive need in the crypto sector to piggyback on the credibility provided by the unit of account issued by the central bank. In this sense, stablecoins are the manifestation of crypto’s search for a nominal anchor.”

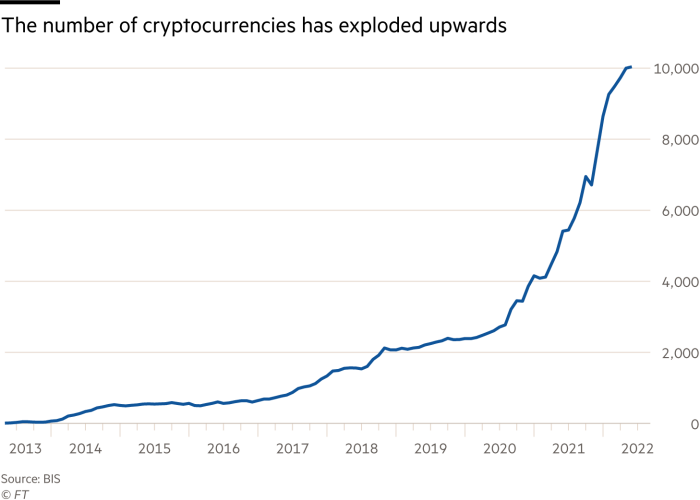

Yet their failings are deeper than that. There are now some 10,000 cryptocurrencies. There could just as well be 1bn. But this tendency to fragment, “with many incompatible settlement layers jostling for a place in the spotlight”, is, the BIS argues, inherent in the system’s economic logic, not just its technological ability to multiply without limit.

In a good monetary system, the greater the number of users the lower the costs of transactions and so the greater its utility. But, as more people use a cryptocurrency, the greater the congestion and the more costly the transactions. This is because self-interested validators are responsible for recording transactions on the blockchain. The latter must be motivated by monetary rewards high enough to sustain the system of decentralised consensus. The way to reward validators is to limit the capacity of the blockchain and keep fees high: “So, rather than the familiar monetary narrative of ‘the more the merrier’, crypto displays the property of ‘the more the sorrier’.”

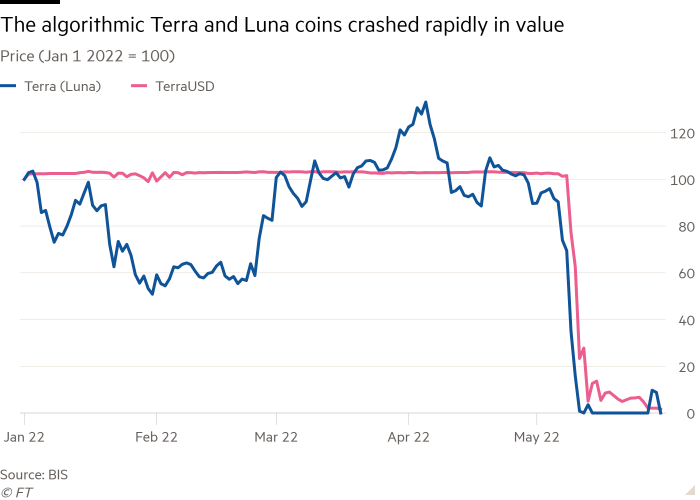

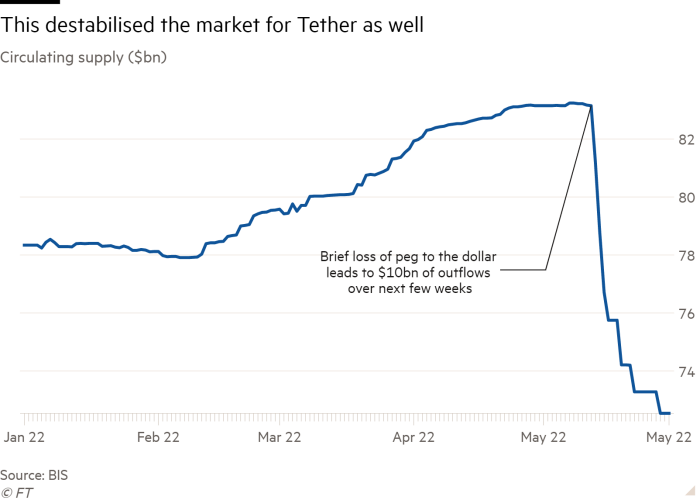

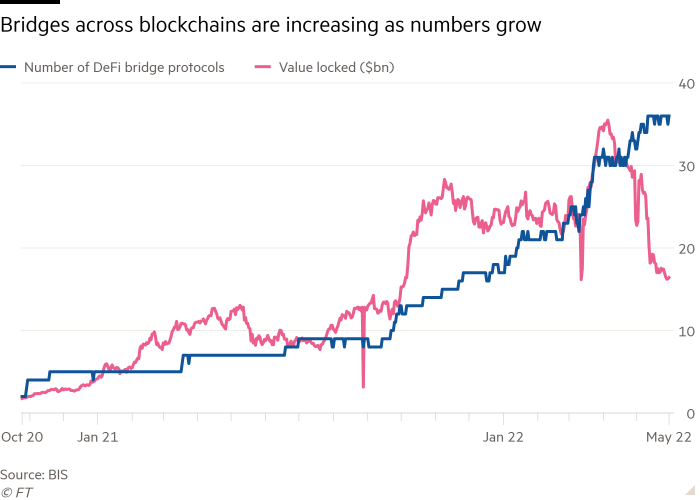

One cannot have all three of security, decentralisation and scalability. In practice, cryptocurrencies sacrifice the last. The crypto system gets round this handicap with “bridges” across blockchains. But these are vulnerable to hacks. The BIS’s conclusion then is that: “Fundamentally, crypto and stablecoins lead to a fragmented and fragile monetary system. Importantly, these flaws derive from the underlying economics of incentives, not from technological constraints. And, no less significantly, these flaws would persist even if regulation and oversight were to address the financial instability problems and risk of loss implicit in crypto.” A fragmented monetary system is not what we need.

What then is to be done? Part of the answer is to insist that crypto meets the standards expected of any significant part of the financial system. Among other things, exchanges must “know their customers”. Again, the assets and liabilities of so-called “stablecoins” should be transparent. Links between banks and crypto players must be particularly transparent.

Yet we can do better than that, argues the BIS. What we need from a good monetary system are safety, stability, accountability, efficiency, inclusion, privacy, integrity, adaptability and openness. Today’s system falls short, especially on cross-border payments. The BIS envisages in its place a system in which central banks would continue to provide payment “finality” on their balance sheets. But new branches could grow on the central bank’s trunk. Above all, central bank digital currencies (CBDCs) could permit a revolutionary restructuring of monetary systems.

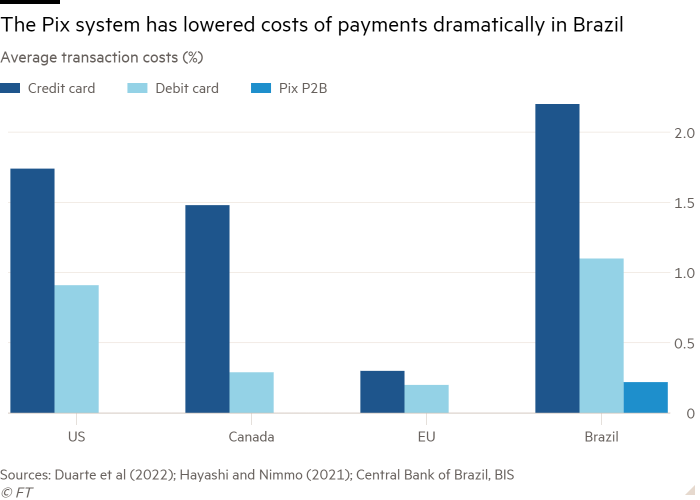

Thus, wholesale CBDCs could offer new functions for payment and settlement to a much wider range of intermediaries than domestic commercial banks. A key element, suggests the BIS, would be the possibility of executing “smart contracts”. Such changes would allow creation of new, substantially decentralised payment systems. Meanwhile, retail CBDCs could complement the development of the new fast payment systems, which are challenging the rents of incumbents. The BIS points to the success of the new Brazilian system, Pix. But full benefits would only be achieved from these if CBDCs were to revolutionise cross-border payments.

Retail CBDCs would also permit a substantial separation of payments from risk-taking. Thus the money that businesses and households hold for transaction purposes could become the liability of central banks. Payments would then be managed by companies that focus on this function, which would make their profits from transactions rather than lending. We would then no longer need the state’s explicit and implicit insurance of private banks. Instead of managing payments, the latter would focus on lending. Their liabilities could also become less liquid and more obviously risk-bearing than they are now. This would indeed be revolutionary.

Yet there are also more modest options. The fundamental point is that the crypto universe does not provide a desirable alternative monetary system. But technology can and should do so. Central banks must play a central role in facilitating a system that protects and serves people better than today’s.

It is time to prune the crypto thicket. But new branches must also grow on the tree of money and payments.