This story is part of State of Emergency, a Grist series exploring how climate disasters are impacting voting and politics. It is published with support from the CO2 Foundation.

During the presidential debate earlier this month, Vice President Kamala Harris was asked about her plan to fight climate change. Her response didn’t focus on the dangers of drought or rising sea levels, or unveil an ambitious plan to reign in fossil fuel emissions. Instead, her answer focused on home insurance. “It is very real,” Harris said. “You ask anyone who lives in a state who has experienced these extreme weather occurrences who now is either being denied home insurance or it’s being jacked up.”

Just a few years ago, Harris’ insurance comments may have been considered wonky or boring to voters. But since 2020, the increasing number and severity of natural disasters like wildfires and hurricanes have cast home insurance markets into turmoil, leading to an explosive rise in premiums.

Unaffordable premiums now represent one of the most tangible ways that climate change is affecting everyday Americans. And this election season, insurance commissioners — the state officials in charge of overseeing these markets — are suddenly in the hot seat.

These officials have historically operated outside of the spotlight, steeped in financial statements and wonky regulations. In the 11 states that elect their commissioners — the rest appoint them — these races have rarely received much interest. In some elections, incumbents don’t even face a challenger. In others, state data shows that as many as 17 percent of voters simply skip over that section of their ballots.

“It’s just not something [voters] pay attention to until things go wrong,” said Dave Jones, who served as California’s insurance commissioner from 2011 to 2019. “Right now, things are going wrong.”

In recent years, insurance companies have found themselves increasingly on the hook for homes hit by wildfires and severe storms. In Louisiana, a parade of back-to-back hurricanes and extreme storms in 2020 and 2021 caused insurers to pay out well over twice as much money as they brought in. Similarly, in Colorado, where the state has experienced over 40 billion-dollar disasters in the past decade, insurers lost money in eight of the past 11 years.

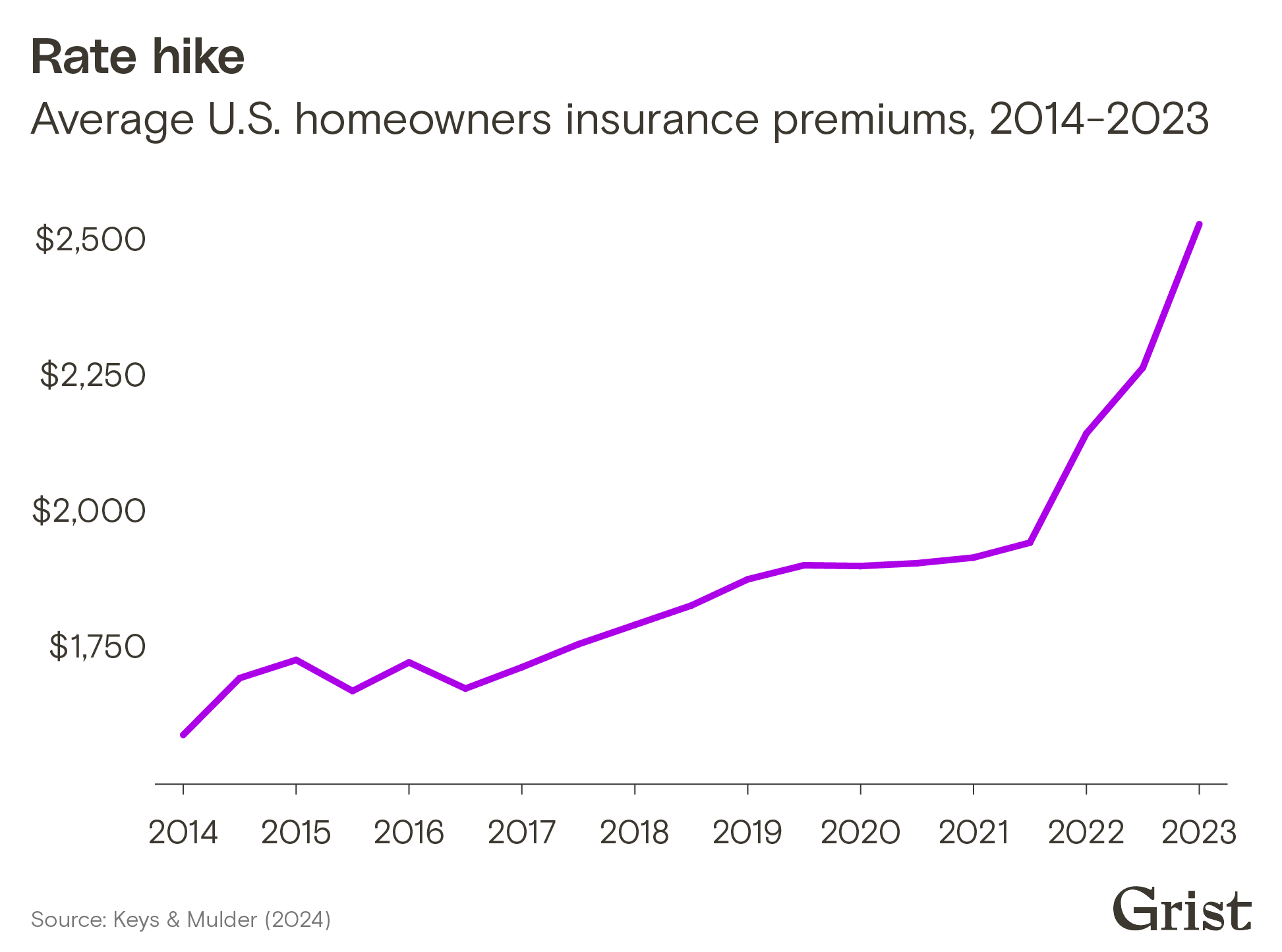

To pay for all this damage, premiums have been skyrocketing nationwide. According to a 2024 study of insurance rates, the average home premium rose 33 percent between 2020 and 2023. In disaster-prone areas like Florida, the Gulf Coast, and California, rates have increased even more, with some insurers pulling out of markets entirely.

“The insurance crisis that people and businesses are experiencing — not just in California, but across the United States — is the price that we’re paying for failure to more aggressively transition from a fossil fuel-based economy,” Jones said.

These rising costs are prompting voters to take a closer look at elected commissioners that regulate the industry in their home states — and it is forcing candidates to more thoroughly consider insurance shifts and climate change in their platforms.

States have been regulating their insurance markets for more than 150 years, with New Hampshire appointing the nation’s first commissioner in 1851. These regulators are tasked with setting reasonable limits on how much insurance companies can charge for home, car, health, and life insurance. They also oversee how insurers manage their money, so they have enough to pay their bills when disaster strikes. For the vast majority of their history, insurance commissioners haven’t thought much about climate change.

“When I came in, climate change was kind of a footnote,” said Mike Kreidler, Washington’s outgoing insurance commissioner, who was first elected to the office in 2000. “That was something that bothered me a lot, because I saw the risks.”

Kreidler’s early attempts at climate action were met with fierce resistance. As an early member of the National Association of Insurance Commissioners’ climate working group, he recalled some of his peers asking him to remove the word “climate change” from his proposals. “I took a lot of abuse back then on these issues,” Kreidler said. “It’s not something that a number of commissioners wanted to talk about.”

Even in progressive states, climate change was often overshadowed by flashier issues. In California, Jones first ran for office in the wake of the newly passed Affordable Care Act. He and his 2010 opponent both campaigned almost entirely on health care issues.

But by Jones’ second term, it was clear things were changing. California was starting to see a worrying trend of expensive wildfires: Starting in 2015, California was hit with billion-dollar wildfires every year until 2023. One of the most tragic examples came in 2018, when the Camp Fire devastated the Northern California town of Paradise, leveling entire neighborhoods and displacing more than 50,000 residents. Jones spent his final year in office making sure fire victims received the claims they were owed, and writing recommendations to protect the system against future disasters.

AP Photo / Eric Risberg

Soon, other states joined California in starting to feel the effects of climate change on the insurance market. In 2021, home premiums — which had remained relatively stable until then — dramatically started to spike nationwide. Insurance commissioners could no longer afford to ignore the impacts of worsening extreme weather. Some candidates, like Delaware’s incumbent insurance commissioner Trinidad Navarro, have called climate change one of the most concerning issues going forward. It’s “become a number one issue for insurance regulators across the United States,” Jones said.

It has become an important issue for voters as well. Over the last few years, major insurance companies have started backing out of high-risk parts of the country. California’s largest insurer, State Farm, stopped accepting new customers, and will not renew policies for roughly 30,000 homeowners and renters living in certain risky parts of the state. Meanwhile, in Florida, so many homeowners have been denied coverage that the government-created “last-resort” program is now the largest insurance provider in the state. This trend — of fewer and more expensive options — is leading some frustrated voters to turn their attention toward their elected leaders.

This year, North Carolina has become the battleground of one of the nation’s first insurance commissioner races centered largely around climate impacts. Coastal storms and hurricanes are taking a worsening toll on the state — like Hurricane Florence, which caused over $16 billion in property damage in 2018. In response, North Carolina insurers requested a 42 percent increase in home insurance rates. In certain coastal neighborhoods, they asked for a rate increase of 99 percent.

This proposal was met with fury: Insurance commissioner Mike Causey, a Republican, received more than 24,000 emails, and a public comment session held earlier this year was filled with roughly seven hours of angry testimony, from small town mayors to ordinary homeowners. Senior citizens feared that their social security income wouldn’t cover their new premiums, and local military families worried that their housing allowances would also fall short. Realtors worried the new rates would deal a devastating blow to the state’s housing market. Causey eventually rejected the initial proposal, calling them “excessive and unfairly discriminatory,” but has yet to settle on new insurance rates. Causey did not respond to multiple interview requests.

For Natasha Marcus, a Democratic state senator challenging Causey in the election this year, this public outcry has brought a lot of attention to the commissioner race. According to an August poll from the group Carolina Forward, Marcus and Causey are currently neck-and-neck. “It’s the sexiest race on the ballot,” Marcus said, half jokingly. “As soon as people realize how directly it impacts their wallets, they take an interest.”

Marcus is hoping for more transparency in the rate-setting process, to give customers a better sense of whether premium hikes are truly justified. Her vision is for a courtroom-like procedure, where insurers can make their case to the public, and her office can cross-examine their arguments.

AP Photo / Karl B DeBlaker

While Marcus acknowledges the threat of climate change, she feels that North Carolina insurers are using extreme weather as a pretext to ask for unreasonably high rates, pointing to a New York Times investigation that shows the state’s insurers have made profits 10 of the past 11 years. She worries that large insurance companies are seeking easy profits from North Carolina to make up for the money they’re losing in other states.

A 2022 Federal Reserve analysis found that insurers are indeed quicker to ask for rate hikes in states with looser insurance regulations, and more hesitant in highly regulated states like California — even if those states experience frequent disasters.

However, Ben Keys, an economist and professor of real estate and finance at the University of Pennsylvania’s Wharton School, says that this trend does not explain the recent hike in insurance costs. He and a colleague recently analyzed premiums from 47 million homeowners across the country, revealing an unprecedented view into the causes of the insurance crisis.

Over the past 40 years, Americans have been moving to more disaster-prone regions of the U.S. South and West. “A hurricane cutting the Gulf side of Florida now just encounters way more houses, way more businesses, way more roads, way more infrastructure than it did 40 years ago,” Keys said.

At the same time, climate change has been increasing the frequency and severity of extreme storms and wildfires in those fast-growing regions. Finally, when disaster strikes, inflation and labor shortages have driven up the cost of rebuilding.

All of these factors have made disasters more expensive, and contributed to the rise in premiums. But the biggest factor behind the rise, according to Keys, is the way that climate change is reshaping a fundamental pillar of the insurance industry.

Insurance is built around the assumption that disaster doesn’t strike everyone at the same time. For many types of insurance, that assumption is mostly true — a car insurer, for example, knows that it’s unlikely that every driver will get into a fender bender on the exact same day. But when it comes to home insurance, climate change is causing this assumption to crumble. A major wildfire could easily burn down an entire town, or a hurricane could easily rip the roofs off all the homes in a neighborhood. For this reason, insurance companies in disaster-prone regions end up purchasing their own insurance policies, known as “reinsurance.”

Reinsurance protects regular insurance companies from going bankrupt from a string of major disasters. Since reinsurance companies cover the epicenters of extreme weather, they’ve recently become extremely sensitive to climate risk. Since 2020, premiums for reinsurance have doubled, and will likely continue to rise. In states that experience frequent extreme weather disasters — like Louisiana, Texas, and Florida — insurance companies end up purchasing a lot of expensive reinsurance, and those costs get passed down to customers.

This is the biggest factor behind the recent surge in home insurance premiums, and Keys doesn’t expect it to stop anytime soon. In a recent interview with Bloomberg, Jacques de Vaucleroy, the chairman of the major reinsurance firm Swiss Re, said that reinsurance premiums will continue to rise until people stop building in dangerous areas.

This puts candidates like Marcus in a difficult position. Voters may hate high insurance rates, but they also love their state’s beautiful coastline. “It is not a solution to say, ‘Well, there will just be no houses on the coast anymore,’” Marcus said. “Nobody wants that.”

Mark Wilson / Getty Images

Keys thinks that insurance commissioners will have to make some difficult and unpopular decisions going forward. He worries that elected commissioners might choose to please voters in the short term, instead of addressing the root causes.

“It’s very fraught to have an elected official in charge of regulating this market,” Keys said. “If you set prices too low, then you make voters happy — but at the cost of not reflecting the true risk. That’s going to encourage people to build more in risky areas.”

While Marcus believes the rate hikes proposed earlier this year in North Carolina were unjustified, she acknowledges that climate change will inevitably cause rates to increase in the future. “I never promise that I will never raise your rates if you elect me,” Marcus said. “It sounds really good on the campaign trail, but I tell the truth. And the truth is, sometimes rates do need to go up.”

Instead, Marcus hopes that more transparency would keep insurers honest, and her campaign pledges to push for more adaptation and resilience. For example, North Carolina’s high-risk insurance program offers grants to policyholders to storm-proof their roofs. Marcus would like to see more resources devoted to that program. “If the hurricane comes through and your roof stays on, you’re going to have a lot less damage,” Marcus said. “That helps reduce insurance costs for everybody.”

This is something that insurance commissioner candidates in other states are pushing for as well. In Montana, a state that over the past decade has averaged 7.2 million acres burned annually, Republican candidate James Brown has called for insurance incentives for homeowners who implement fire resilience measures to their homes. In Washington, Democratic candidate Patty Kuderer has called for similar plans in her state.

AP Photo / Elaine Thompson

Jones, now the director of the Climate Risk Initiative at the University of California, Berkeley, has been advocating for similar reforms in California since leaving office. In recent years, the state and local governments have been spending millions on prescribed burning and thinning in order to make forests and communities more resilient to wildfires. Jones has been working with lawmakers to make sure California insurers take those investments into account when writing and pricing policies.

In this way, insurance could serve as both a carrot and a stick, discouraging people from building in risky areas, and also rewarding people for making their homes and communities more resilient. But Jones also hopes that voters will put the pieces together.

“If the voters are connecting the dots, they should understand that what they’re experiencing — in terms of increased price and lack of availability of insurance — is driven by climate change, ” Jones said. “They should look to elect an insurance commissioner who’s going to be a leader in addressing the underlying driver of the problem, which is climate change.”